Suggestions and operational recommendations:

South American soybeans were basically scheduled for 17/18, and the market turned to US soybean exports and new seasons of US soybeans. Due to the sharp drop in production of Argentina's soybeans, a substantial and unrecoverable reduction of about 14 million tons of soybeans in South America has caused global soybean supply to shift from loose to tight, and soy prices are significantly more sensitive to supply-side variables, while US new season soybeans If the planting enthusiasm is lower than expected, then the US soybean planting season will not be the slightest problem. In addition, under the influence of bullish expectations, the downstream warehousing enthusiasm will increase, the export of US soybeans is expected to accelerate, digest high stocks, and the probability of lowering the carry-over stocks in the old quarter will increase, which will provide support for the long-term operation of soybeans. China has increased its tariff on the US soybean by 25%. The black swan incident will occur and the price of soybean meal will rise.

Operation strategy:

Strategy: Soybean meal keeps the overall upward trend of the shock, and does more business ideas on dips. Among them, Dalian Pandou is treated as a bargain. There are stock traders, keep a certain amount of stock, the spot can be shipped in arbitrarily high volume, traders without stocks suggest that they can buy near the support position and establish a trade position.

Risk factors:

USDA's inventory continued to increase in April, Argentina's production cuts were less than expected, Brazil's large exports, US soybean planting area is higher than the March intention report.

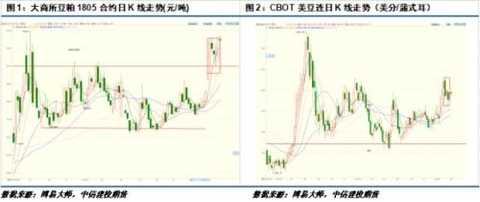

First, the market review

In March, due to the heating friction between China and the United States, the internal and external markets showed a distinct differentiation. In the first half of March, due to the reduction of soybean production in Argentina and the market expectation that the US soybean new crop area will continue to increase, the US soybeans stagnate and fall in the 1080 line, and domestic soybean meal basically follows the trend of the outer disk. However, on March 22, US President Trump signed a memorandum to announce the imposition of a $60 billion tariff on China. The Sino-US trade war started. The market is worried that the trade war may affect US soybean exports. The internal and external disc differentiation is characterized by weak external strength. . As of March 30, the US soybeans closed at 1044 cents per ounce, down 10 cents or 1% from the previous month. The Dalian Beans Bean 05 contract closed at 3,149 yuan / ton, up 141 yuan from last month. The ton or increase is 4.69%.

Second, the price impact factor analysis

2.1 New season US soybean cultivation enthusiasm is lower than expected

The new season's US soybean planting area was unexpectedly lower than expected. The US Department of Agriculture (USDA) announced the planned area of ​​planting in the new season at the end of March. Soybean is expected to be 88.928 million acres, down 1.16 million acres from the actual area of ​​90.142 million acres last year, down 1.29%, and unexpectedly lower than the market average of 90.919 million acres. .

We believe that the main reasons for the planting area being less than expected are:

1) US soybean 17/18 soybean exports are not very optimistic, and the export progress is significantly behind the five-year average.

2) The price of US soybeans is low, and the enthusiasm of farmers is not strong.

3) Sino-US trade war risk, because one-third of China's imported soybeans come from the United States, fearing that China's retaliatory tariffs on US soybeans will seriously hit US soybean exports.

4) Due to the increasing probability of continuous planting of soybean diseases and pests, the necessity of rotation is receiving increasing attention.

We can see that the market expectation has shifted from a slight expansion to a large contraction. This expectation will provide a favorable environment for the medium-term trend of the US soybean. Since the mid-April to the end of June is the US soybean planting period, attention will be paid to the progress of planting in key states, and the USDA will announce the planting area at the end of June. According to the data of the past 17 years, in the context of the reported area decreased by more than 1% in March, the reported area in June continued to decline three times in March, with a decrease of 0.82-4.55%, which was basically the same as that in March. It is only one time higher than that in March (an increase of 2.95%). Combined with the above data, we believe that the area will continue to decline in June this year, with an estimated area of ​​8720-8825 million acres and a minimum limit of 84.93 million acres.

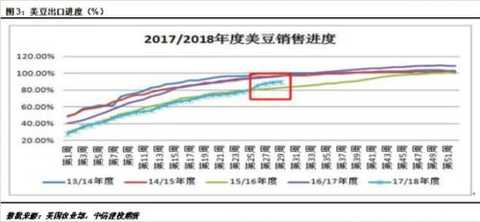

2.2 US soybean export speed accelerated to digest high inventory

US 17/18 soybean stocks were high in the quarter. As of March 1, US soybean stocks were 2.107 billion pu, higher than market expectations of 2.042 billion pu, up 21.16% from 1.739 billion pu in the same period last year, mainly to China soybeans. Drastically reduced, squeezed by Brazilian beans. As of March 22, the total US soybean export sales to China in the 17/18 year has decreased by 18.1% compared with the same period of the previous year. The total sales volume was 28.537 million tons, which was 3.31 million tons lower than the 34.47 million tons in the same period of last year. China's soybean export shipments were 25.865 million tons, down from 32.575 million tons in the same period of the previous year. The number of unloaded soybeans was 2.672 million tons, compared with 2.272 million tons in the same period last year.

Although the overall sales progress of the US soybeans was lagging behind, in March, the weekly sales of the US soybeans increased and the export speed accelerated, and the export expectations began to improve. As of the week of March 22, the cumulative sales of soybeans was 4.86 million tons, an increase of 124% compared with 2.17 million tons in the same period of last year. The cumulative export was 3.23 million, higher than the 3.51 million tons in the same period of last year, an increase of 2.54%. The USDA export target was 89.59%, which was lower than the five-year average of 94.2%, lower than last year's 96.77%.

As of March 22, according to the USDA March supply and demand report export target, the 17/18 US soybeans still need to export 15.2 million tons of soybeans. In the quarter, the US soybeans have a 23-week export time window, and the weekly soybean export volume needs to reach 660,900. Tons can be achieved (the average of last year was 498,900 tons/week). The average export value of US soybeans in March was 807,300 tons, higher than the 786,600 tons in the same period of last year. It is also obvious that export expectations are starting to improve.

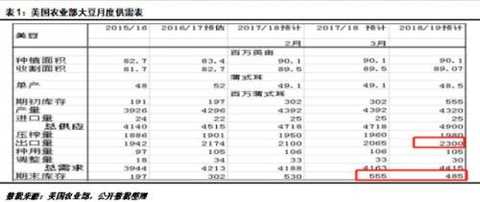

2.3 US soybean carryover stock inflection point has a high probability of occurrence

In the 2018/19, the US soybean stocks had a higher probability of decline than the previous year, or ended the three-year inventory growth pattern. According to the USDA Supply and Demand Outlook report, US soybeans are expected to carry over 485 million bushels in 18/19, down from 555 million bushels in 17/18, mainly due to a sharp increase in export forecasts. USDA can significantly increase exports to 2.3 billion bushels, an increase of 235 million bushels (about 6.4 million tons), mainly due to the substantial reduction in soybean production in South America in 17/18 (estimated production cuts of 14 million tons), mainly due to the sharp reduction in production in Argentina. Instead of Argentina's about 6-7 million tons of soybean exports.

2.4 South America's basic production cuts

Brazil's 17/18 soybean production continues to be high. Forecasting institutions have raised Brazilian soybean production forecasts, and consulting firm Agroconsult expects Brazil's soybean production to reach 119 million tons this year, as yields in the main producing areas increase, and INTL Fcstone expects Brazil's 2017/18 soybean production to be 1.159. Billion tons, up by 2.7% from March, USDA is expected to be 113 million tons in March, up 1 million tons from February.

Argentina’s sharp cut in 17/18 is a foregone conclusion. Due to the extreme drought in the soybean growing season in Argentina and the severe damage to soybeans in 40 years, the exchange expects the predicted soybean production in Argentina in 17/18 to be 39.5 million tons, which is lower than the previous forecast of 42 million tons, which is lower than the initial forecast. The value is 14.5 million tons lower than the 57.5 million tons in 2016/17.

In summary, the 17/18 South American soybeans experienced a substantial and unrecoverable reduction of about 14 million tons, which made the global soybean supply shift from loose to tight, and the soybean price was significantly more sensitive to supply-side variables, while the US new season soybean cultivation If the enthusiasm is lower than expected, then the weather of the soybeans in the growing season will not be the slightest problem. In addition, under the influence of bullish expectations, the downstream warehousing enthusiasm will increase, the export of US soybeans is expected to accelerate, digest high stocks, and the probability of lowering the carry-over stocks in the old quarter will increase, which will provide support for the long-term operation of soybeans.

2.5 In the second quarter, the arrival of soybeans in Hong Kong is abundant

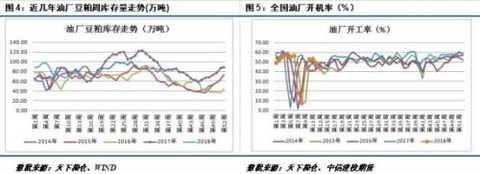

In March, soybeans arrived in Hong Kong at 5.662 million tons, up from 5.64 million tons in February, lower than the previous forecast of 6.05 million tons, mainly due to the delay of some shipments to April. Due to the unexpected arrival of soybeans in Hong Kong in March, port inventories fell back. As of March 30, the stock of soybean ports was 6,627,800 tons, down 2.13% from the end of last month. As the current oil mill crushing profits are very rich, oil mills purchase a large number of long-term soybeans. It is estimated that the soybeans arriving in Hong Kong in the second quarter will be 27.67 million tons, an increase of 6.96% compared with 25.87 million tons in the same period last year. According to the world granary network: April is expected to reach 8.07 million tons of soybeans in Hong Kong, 9.6 million tons in May and 10 million tons in June.

Due to the active return of the oil plant after the Spring Festival, the weekly crushing volume has recovered to 1.8 million tons. Even though some oil mills have been repaired and crushed in the middle and late seasons (1.48 million tons/week), the overall supply is loose. As of March 30, the coastal areas are mainly The stock of soybean meal in oil plants was 770,000 tons, an increase of 60,000 tons from the 710,000 tons at the end of last month, an increase of 8.45%. As there is Ching Ming Festival in the first week of April, the recovery rate is not obvious. It is estimated that after the middle of April, the oil plant will resume its work, and the oil plant crushing volume is expected to return to the level of 1.7 million tons per week. The supply pressure will be reappeared. The price can continue to be insufficient.

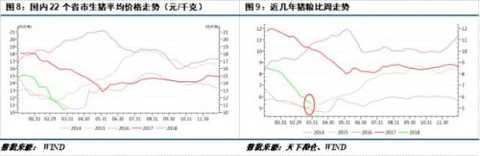

2.6 Soybean meal demand is not easy to be excessively pessimistic

Since the beginning of the year, the hog market has been covered with a haze, and in March, the domestic pig price has reached a new level, hitting a new low since 2014, but the monthly decline has narrowed. According to China Animal Husbandry Network, as of the end of March, the average price of live pigs in 22 provinces was 10.49 yuan / kg, down 1.51 yuan / kg from 12 yuan / kg at the end of February, a decrease of 12.58% (19.52% last month), compared with 15.89 in the same period last year. Yuan/kg fell 33.98%; the average price of pig food fell from 6.56:1 last month to 5.48:1, with a monthly decline of 16.77%, down 46.06% from 10.16:1 in the same period last year. In March, the price of eggs fell weakly. As of March 30, the market retail egg price was 6.9 yuan/kg, down 1.1 yuan from 8 yuan/kg at the end of February, a decrease of 13.75% (previous month's decline of 11.89%), compared with 5.68 in the same period last year. Yuan/kg rose 21.48%.

Due to the rising cost of raw materials, the domestic feed price rose in March. The price of corn was 1.89 yuan/kg, up 0.5% from the previous month and up 17.4% year-on-year. The price of soybean meal was 3.17 yuan/kg, up 3.2% from the previous month and up 8.9 from the same period last year. %, the price of finishing pigs was 2.63 yuan / kg, up 1.5% from the previous month and up 5.6% year-on-year.

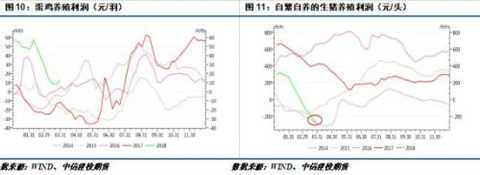

In March, the profit loss of the aquaculture industry continued to deteriorate. Among them, the loss of pig breeding returned to the low level in 2014, and the laying of laying hens fell from the previous month, which was at a high level of nearly five years. As of March 30, the profit from self-supporting pigs was negative at 269.32 yuan/head, down by 36.36 yuan/head from the end of last month, down 378% from the previous year's 423.85 yuan/head; the laying rate of laying hens fell back to 13.08. Yuan/Feather, down 26.81 yuan/feather from the end of last month, down 51%, up 214% from the same period last year, minus 11.52 yuan / feather.

At present, the price of live pigs continues to be weak, and the loss of farming is serious. In addition, the current feed price rises and the risk of breeding increases. Farmers are more pessimistic about the market outlook, and the replenishment is not active, and the price of piglets continues to weaken. However, due to the low prices of farmers at the end of the month, the price of live pigs stopped falling and rebounded, and some farmers increased their wait-and-see mood. In general, due to the serious losses in the aquaculture industry, the supply of pigs is abundant. The demand for feed in the growing season is increasing. The demand for soybean meal is stable. The loss only affects the piglets, but there is no market expectation. Pessimism. Combined with the impact of rising feed costs on market sentiment, downstream feeds are worried that raw materials will continue to rise or actively stock up in advance. Overall, demand for soybean meal in April is stable.

Third, China imposes a 25% tariff on US beans.

At 4:55 pm on April 4, the State Council Customs Tariff Commission decided to impose a 25% tariff on soybeans originating in the United States. This measure will support the domestic soybean meal price to rise sharply. According to the price quoted in the morning, the cost of imported US soybeans in April-November is 3242-3338 yuan/ton. Considering the 25% tariff increase, the enterprise cost will increase by 810-845 yuan per ton, and the cost will be directly transferred to soybean downstream goods. . Estimated cost per ton of soybean meal increased by 19.6%, calculated by the average price of coastal spot soybean meal 3200 yuan / ton, the price per ton of soybean meal rose 627 yuan, then the settlement price of Dalian M05 was 3149 yuan / ton, the settlement price of M09 was 3193, the settlement price of M01 3213, the corresponding target price is 3776, 3820 and 3840 respectively. Since futures volatility is more intense than the spot price, and the market sentiment is affected, the actual value should be higher than the target price. Later, I paid attention to the trend of US soybean prices and South American spreads.

4. Outlook and strategy

At present, South American soybeans are basically scheduled for 17/18, and the market turns to the export of US soybeans and the sowing of new seasons. Due to the sharp drop in production of Argentina's soybeans, a substantial and unrecoverable reduction of about 14 million tons of soybeans in South America has caused global soybean supply to shift from loose to tight, and soy prices are significantly more sensitive to supply-side variables, while US new season soybeans If the planting enthusiasm is lower than expected, then the US soybean planting season will not be the slightest problem. In addition, under the influence of bullish expectations, the downstream warehousing enthusiasm will increase, the export of US soybeans is expected to accelerate, digest high stocks, and the probability of lowering the carry-over stocks in the old quarter will increase, which will provide support for the long-term operation of soybeans. China has increased its tariff on the US soybean by 25%. The black swan incident will occur and the price of soybean meal will rise.

Domestically, due to the huge profits from crushing, the amount of soybeans arriving in Hong Kong in the second quarter hit a new high in recent years. With the increase in the operating rate in April, supply pressure will once again show up, and the price of spot soybean meal will continue to be insufficient. In the context of South American production cuts, the price of long-term soybean meal is affected by the weather risk and trade risk of the new season, and it is easy to rise and fall. The medium-term center of gravity fluctuates upwards. In terms of arbitrage, the basis of the near-month and far-month will continue to weaken.

Strategy: Soybean meal keeps the overall upward trend of the shock, and does more business ideas on dips. There are stock traders, keep a certain amount of stock, the spot can be shipped in arbitrarily high volume, traders without stocks suggest that they can buy near the support position and establish a trade position.

Risk warning: USDA's inventory continued to increase in April, Argentina's production cuts were less than expected, Brazil's large export, US soybean planting area was higher than the March intention report.

Baby Bedding Products,Baby Sleeping Bag Products,Baby Pillow,Children'S Pillows

USHARE INDUSTRIAL (DONGGUAN)CO.,LTD , https://www.usharedg.com